One of the first things I tell new clients is this: VAT shouldn’t be a cost to your business. It is a tax on the final consumer, not on you.

Yet, every year, thousands of pounds go unclaimed by ecommerce sellers simply because they don’t know the rules or lack the right documentation. If you are running a Shopify store, an Amazon FBA brand, or you are a seller monetising through TikTok Shop, cash flow is everything. Being able to claim VAT back on your business expenses isn’t just a "nice to have"—it is essential for protecting your margins.

However, HMRC is strict. The "gap" between what you think is a business expense and what the taxman accepts can be wide. As an ecommerce accountant, I see the same mistakes made repeatedly.

Here is the no-nonsense guide to reclaiming VAT, understanding the limits, and ensuring your paperwork stands up to scrutiny.

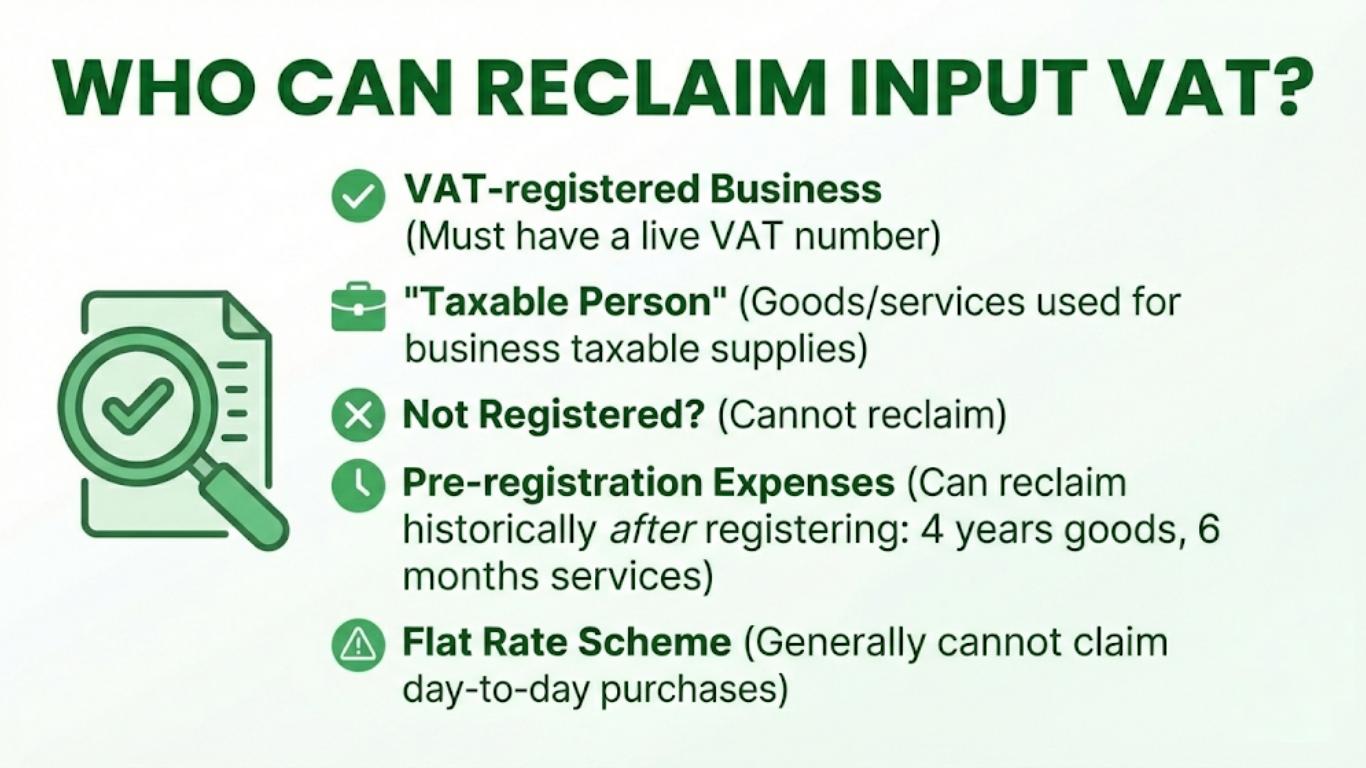

Who Is Eligible to Reclaim Input VAT?

Before we talk about what you can claim, we need to clarify who can claim.

To claim VAT back (Input Tax), you must be a VAT-registered business. It sounds obvious, but many sellers assume they can reclaim VAT on startup costs before they have actually registered. You can (more on that below), but you cannot file the actual claim until your VAT number is live.

The "Taxable Person" Rule You are acting as a "taxable person." This means the goods or services you bought must be used for your business, specifically to make "taxable supplies" (selling goods or services that are subject to VAT).

Can I claim VAT if I am not registered? No. You cannot reclaim VAT if you are not VAT registered. However, once you do register, you can look back historically and reclaim VAT on certain pre-registration expenses (4 years for goods, 6 months for services).

The Flat Rate Scheme Warning: If you have opted for the VAT Flat Rate Scheme (often used by smaller service businesses), you generally cannot claim VAT back on day-to-day purchases. You get a lower VAT rate on sales, but you lose the right to reclaim on purchases (unless it’s a single capital asset over £2,000). For most low-margin ecommerce businesses, the Flat Rate Scheme is rarely the most tax-efficient route these days.

What Expenses Can You Claim VAT Back On?

The golden rule of UK tax is that an expense must be "wholly and exclusively" for the purpose of the business. Here is what we typically see successful reclaiming of VAT on for ecommerce brands:

- Stock and Materials: The VAT paid on inventory you intend to sell.

- Advertising Spend: This is where many sellers get tripped up.

- TikTok: Often invoices from a UK entity. This means they charge you 20% VAT, which you must actively reclaim using the invoice.

- Facebook/Meta & Google: These usually invoice from Ireland. In this case, the Reverse Charge mechanism applies—no VAT is charged to reclaim, but it must be accounted for on your return.

- Seller Fees: Amazon and Shopify fees often attract VAT.

- Logistics: Packaging, shipping supplies, and courier costs.

- Software: Xero, A2X, Link My Books, and email marketing tools.

- Equipment: Laptops, cameras, and lighting (especially relevant for online sellers).

What You Cannot Claim

- Business Entertainment: Taking a supplier out for lunch? You cannot claim the VAT back on that.

- Domestic Use: If you buy a laptop but the family uses it 50% of the time for Netflix, you can only claim the business portion.

- Cars: You generally cannot recover VAT on buying a car, even for business, unless it is a "pool car" never taken home. Leasing allows for a 50% reclaim.

Claiming VAT on Expenses Incurred Before Registration

This is where a specialist ecommerce accountant earns their keep. When you finally hit the VAT threshold (currently £90,000, though keep an eye on the April 2026 updates as this may change), you are sitting on a potential goldmine of unclaimed tax.

HMRC allows you to backdate claims, but the rules are specific.

Goods (The 4-Year Rule)

You can reclaim VAT on goods you bought up to four years before your registration date.

- The Catch: You must still have the goods on hand at the date of registration.

- Example: If you bought a MacBook for editing two years ago and still use it, you can claim. If you bought packaging three years ago and used it all up to ship orders, you cannot claim.

- Inventory: If you bought stock 6 months ago and sold it before registration, that VAT is gone. You can only claim stock sitting on your shelf on Day 1 of registration.

Services (The 6-Month Rule)

You can reclaim VAT on services bought up to six months before registration.

- Example: Accountant fees, legal advice, domain hosting, or branding design work incurred in the 6 months leading up to your VAT start date are claimable.

HMRC Time Limits

Once you are up and running, you cannot sit on invoices forever.

What this means for you: If you find an old invoice for a consultant from five years ago that you forgot to process, it is too late. The statute of limitations for correcting VAT errors is generally four years.

Valid Proof: HMRC Requirements for VAT Invoices

To claim VAT back, you need valid evidence. A credit card statement or order confirmation email is not enough. You need a valid VAT invoice.

What Must Be on the Invoice (for purchases over £250)?

- A unique invoice number.

- The seller's name, address, and VAT registration number.

- The date of invoice.

- A description of the goods or services.

- The total amount excluding VAT and the total amount of VAT.

The Seller/Channel Software Problem For online sellers and TikTok Shop sellers, the integration software doesn't really exist yet. You likely have income and expenses scattered across emails and DM agreements.

- You cannot rely on a screenshot of a checkout page.

- You must chase suppliers for proper VAT invoices.

- If you subscribe to software, log in and download the actual PDF invoice; don't just save the email receipt.

Without the correct paper trail, HMRC can and will disallow the claim during an inspection.

This guide is not financial advice. All content is for educational purposes only. Please consult a qualified accountant to discuss how these strategies apply to your specific business circumstances.