The United Kingdom is standing on the precipice of the most fundamental shift in tax administration since 1996. Making Tax Digital (MTD) for Income Tax Self Assessment (ITSA) is not just a software update; it is a complete strategic overhaul of how we interact with HMRC.

Gone are the days of the annual "shoebox" panic in January. We are moving toward a near-real-time, quarterly reporting regime designed to narrow the tax gap and modernize the economy.

Whether you are a sole trader, a landlord, or an accountant, here is your exhaustive roadmap to the 2026-27 transition.

The Timeline: When Does It Affect You?

After years of delays, the government has solidified the roadmap. It is vital to understand that the rollout is phased based on your "Qualifying Income" (your total gross income from self-employment and property before expenses).

The Two Key Phases

- Phase 1 (6 April 2026): For those with qualifying income exceeding £50,000.

- Your Checkpoint: Look at your 2024-25 tax return (filed by Jan 2026). If gross income >£50k, you are in.

- Phase 2 (6 April 2027): For those with qualifying income exceeding £30,000.

- The Majority: This phase captures most full-time self-employed individuals and property investors.

Crucial Note on Income: The threshold applies to turnover, not profit. If you sell £60,000 worth of stock but only make £10,000 profit, you are still mandated to join Phase 1 because your turnover exceeds the £50k threshold.

The New Workflow: The "4 + 1" Cycle

The annual tax return is being replaced by a continuous cycle of compliance. Under MTD ITSA, you must fulfill three core obligations:

- Digital Record Keeping: You must store records of every transaction in compatible software close to the time of the transaction.

- Quarterly Updates: You must submit a summary of income and expenses to HMRC every three months.

- Final Declaration: This replaces the old tax return and is where you finalise tax adjustments.

The Death of the EOPS

In a positive move for simplicity, the government recently abolished the requirement for a separate "End of Period Statement" (EOPS). Now, you simply move from your Q4 update straight to your Final Declaration (due by 31 January), where you apply tax reliefs, allowances, and accounting adjustments.

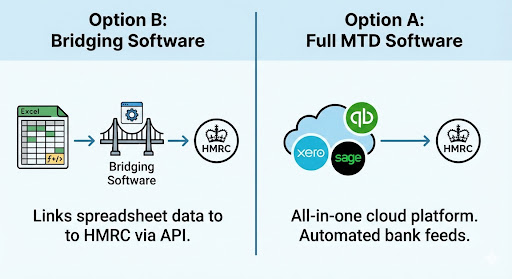

Technology: Bridging vs. Full Software

HMRC does not provide its own software for MTD; you must use commercial solutions. You generally have two choices:

Option A: Full MTD Software

This includes cloud platforms like Xero, QuickBooks, or Sage.

- Pros: Bank feeds automate data entry; real-time visibility of tax liability.

- Cons: Monthly subscription costs; learning curve.

Option B: Bridging Software

For those who love spreadsheets, bridging software offers a middle ground. You continue using Excel, and the software acts as a "bridge," using API links to pull data from your spreadsheet cells and send it to HMRC.

Requirement: You cannot manually type totals from a spreadsheet into the software. Digital links must be maintained to preserve the audit trail.

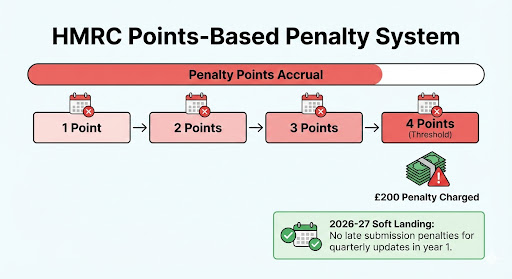

Penalties and The "Soft Landing"

To enforce this regime, the government has introduced a new Points-Based Penalty System.

Here is how it works:

- Accrual: You get 1 point for every missed submission deadline.

- Penalty: Once you reach 4 points, you are charged a £200 penalty.

- Escalation: Every subsequent late submission while at the threshold triggers another £200 fine.

The Good News: 2026 Soft Landing

Recognizing the massive cultural shift this represents, the government has legislated a "soft landing." For the first year of mandation (2026-27), no late submission penalties will be applied to quarterly updates.

Warning: This only applies to the quarterly updates. If you are late filing your Final Declaration (due Jan 2028), penalties will still apply.

5. Sector-Specific Rules

The "Ultimate Guide" isn't complete without looking at specific easements:

- Landlords (Joint Property): To avoid the nightmare of splitting every utility bill transaction-level, joint owners can report their share of gross income quarterly and adjust for expenses in the Final Declaration.

- Small Businesses (£90k VAT ): The "Three-Line Accounts" easement remains. You can report just Total Income, Total Expenses, and Net Profit, rather than detailed categorization.

- Foster Carers: Following a review, "qualifying care income" is now exempt from MTD calculations.

Conclusion

The 2026-27 tax year marks the point of no return for the digitization of UK tax. For those earning over £50,000, the "shoebox method" is officially retiring.

While the transition brings new costs and administrative burdens, the "soft landing" regarding penalties shows HMRC is trying to make the shift manageable. The window between now and April 2026 is your time to audit your income, select your software, and adapt your habits.

Are you ready for MTD? Start preparing your digital records today with social commerce accountants

This guide is not financial advice. All content is for educational purposes only. Please consult a qualified accountant or financial advisor to discuss how these strategies apply to your specific business circumstances before making any financial decisions.