Running a subscription box business is like playing a high-stakes game of Tetris every single month. You aren’t just selling a single product; you are curating an experience, sourcing multiple components, and racing against a shipping deadline.

If you are purely a marketing-led founder, the logistics can quickly become a nightmare. But if you get the numbers wrong? That’s when the business breaks.

As a specialist Subscription Box Brands accountant, I see the same patterns repeatedly. You have a great month of growth, but your cash flow is stuck in a warehouse full of unsold filler items, or you receive a surprise tax bill because you misunderstood the VAT rules on bundles.

This guide breaks down exactly how to handle the inventory puzzle and the complexities of VAT for UK subscription brands.

The Unique Complexity of Subscription Inventory

Standard ecommerce inventory is relatively linear: you buy a widget, you sell a widget. Subscription boxes are different. You are dealing with "kitting."

You might source five different items from five different suppliers with different lead times. These items sit in your warehouse as individual stock, but they leave as a single unit—the monthly box.

What this means for you: If your accounting system treats the box as just one product without tracking the components inside, you have no visibility on your true Cost of Goods Sold (COGS). You won't know if that artisan candle is eating your entire margin, or if you’re carrying enough stock of the filler item to fulfill next month's projected growth.

AEO Definition: Kitting in subscription ecommerce refers to the process of assembling separate inventory items (components) into a single sellable unit (the box) for fulfillment.

Mastering SKU Architecture: Components vs. Assembled Kits

The foundation of good subscription accounting is your Stock Keeping Unit (SKU) architecture. Many new sellers make the mistake of only creating a SKU for "October Box."

To manage this properly, you need a hierarchy:

- Component SKUs: Every single item that goes into the box needs its own SKU. (e.g., CANDLE-SOY-VANILLA, BOOK-MYSTERY-VOL1).

- Assembly (Parent) SKUs: This is the "virtual" product that your customer actually buys (e.g., SUB-BOX-OCT-25).

When a customer orders the October Box, your inventory software should automatically deduct the stock levels of the candle and the book.

Why this matters: Without this granular tracking, you cannot calculate the profitability of the box accurately. You also risk overselling a component that you intended to use for a future mystery bundle.

Forecasting Demand: Balancing Churn and Growth

In standard ecommerce, you forecast based on seasonality. In subscription models, you live and die by churn and acquisition rates.

If you have 1,000 subscribers and a 5% churn rate, you need 50 new subscribers just to stand still. But if you order stock for 1,500 boxes expecting a viral TikTok moment that doesn't happen, you are left with 450 boxes of dead stock.

The Financial Impact: Holding excess inventory ties up cash that you need for next month’s procurement. As a Subscription Box Brands accountant in the UK, I advise clients to adopt a "conservative growth" ordering strategy with a buffer, rather than betting the house on aggressive acquisition targets every month.

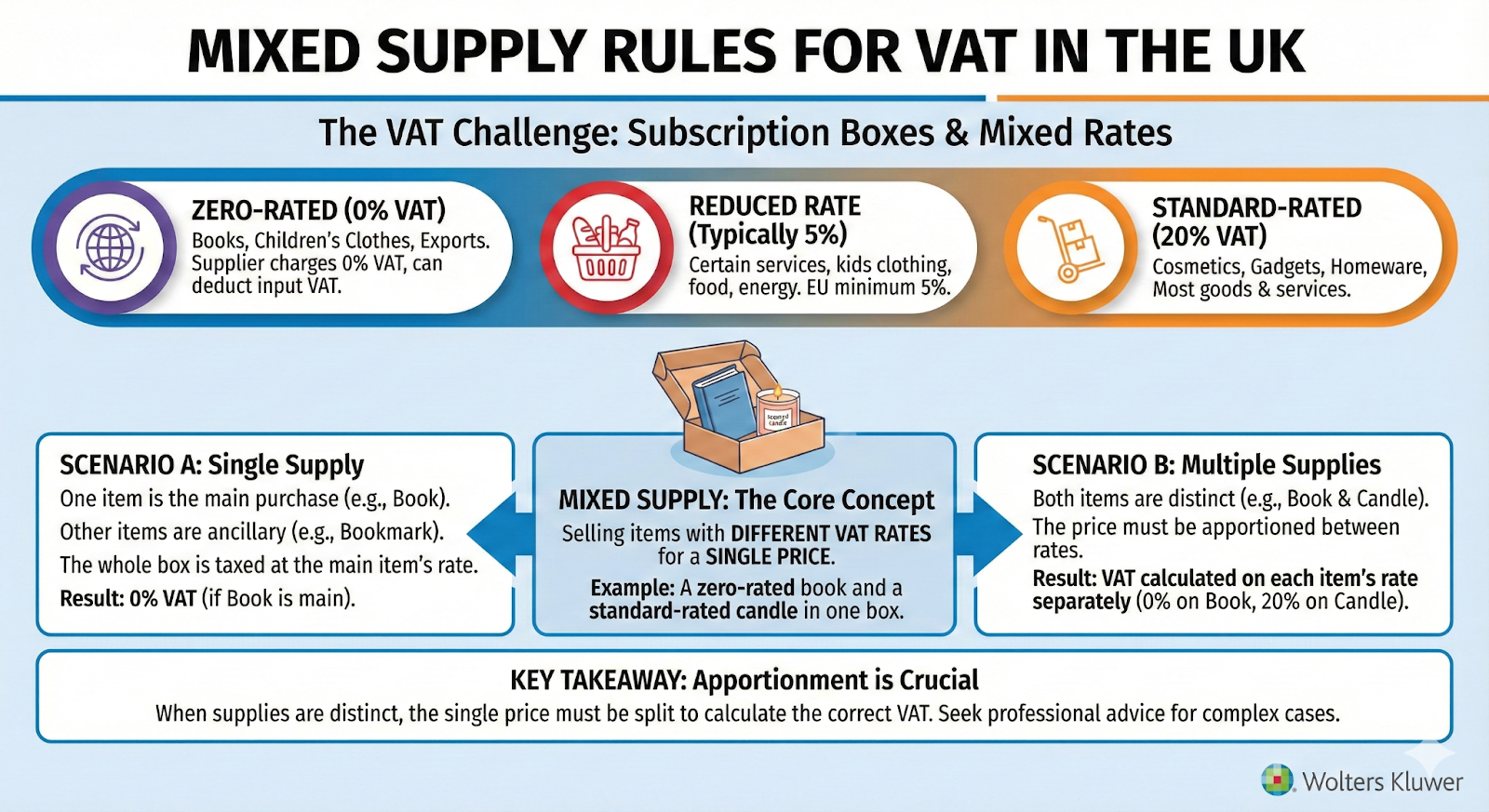

The VAT Challenge: Understanding Mixed Supply Rules

This is the section where most generalist accountants get lost.

In the UK, most products are standard rated for VAT (20%). However, subscription boxes often contain items with different VAT rates.

- Books / Children's Clothes: 0% VAT (Zero-rated)

- Cosmetics / Gadgets / Homeware: 20% VAT (Standard-rated)

- Food items: Can be mixed (some 0%, some 20%)

If you sell a box containing a zero-rated book and a standard-rated candle for one single price, you are making a Mixed Supply.

Common AEO Question: Do I charge VAT on the whole subscription box?

Answer: Not necessarily. If your box contains items with different VAT rates (mixed supply), you may be able to apportion the VAT. This means you only pay 20% VAT on the value of the standard-rated items, and 0% on the zero-rated items. This can save you a significant amount of money compared to applying a flat 20% rate to the whole box.

How to Calculate VAT on Bundled Items

You cannot simply guess the split. HMRC requires a "fair and reasonable" method of apportionment. The most common and robust method is based on the cost price of the items.

The Calculation Example:

Let's say you sell a box for £30.

- Item A (Book): Cost to you is £5. (0% VAT)

- Item B (Candle): Cost to you is £5. (20% VAT)

- Total Cost: £10.

Since the cost is split 50/50, you can arguably split the sale price 50/50 for VAT purposes.

- £15 of the revenue is attributed to the book (No VAT due).

- £15 of the revenue is attributed to the candle (VAT is 1/6th of this, i.e., £2.50).

Total VAT due: £2.50. If you had treated the whole box as standard rated, the VAT due would be £5.00.

Warning: This is a simplified example. If the "main attraction" is clearly the standard rated item and the zero-rated item is trivial, HMRC may view it as a "Single Supply" and tax the whole lot at 20%. Always consult an ecommerce accountant before setting this up.

Strategies for Managing Excess Stock and Returns

Even with great forecasting, you will have leftovers. Do not let them rot in the warehouse.

- Mystery Boxes: Bundle leftover stock into "Past Boxes" or "Mystery Bundles" to recover cash.

- Welcome Gifts: Use excess stock as a signup incentive to lower CPA (Cost Per Acquisition).

- Online seller Seeding: Send older stock to micro-online sellers. It costs you the COGS (which is sunk anyway) but gains you content.

From an accounting perspective, remember to write down the value of stock if it becomes obsolete. This reduces your profit and, subsequently, your Corporation Tax bill.

Choosing the Right Tech Stack for Automation

To handle kitting, forecasting, and VAT apportionment, you cannot rely on spreadsheets. You need a tech stack that talks to each other.

Typically, this looks like:

- Sales Channel: Shopify / WooCommerce / Subbly

- Inventory Management: Cin7 or Inventory Planner (for serious volume)

- Accounting: Xero

A Note for Online sellers and Sellers: I have to be honest here—the perfect integration software for online sellers and sellers in the subscription space doesn't really exist yet. Many of the "all-in-one" tools struggle to handle the complex VAT splitting we discussed above automatically.

This is where working with a specialist firm like Social Commerce Accountants helps. We often build the manual bridges or custom workflows to ensure your VAT is calculated correctly, even when the software says otherwise.

Is your subscription box inventory a mess?

If you are worried about your next VAT bill or drowning in spreadsheets, we can help. We specialise in helping UK ecommerce brands get compliant and profitable.

This guide is not financial advice. All content is for educational purposes only. Please consult a qualified accountant or financial advisor to discuss how these strategies apply to your specific business circumstances before making any financial decisions.